In April, I wrote about a state law that requires the Illinois Comptroller, when requested by a local police or fire pension fund, to intercept state revenue that would otherwise go to the local government and divert those monies to the pension fund instead. The pension funds, starting in 2016, can request this action if a municipality does not make its full, obligated pension payment. It’s important to note that a shortfall in a municipality’s annual pension contribution is different than a pension fund’s overall fiscal condition, which is often discussed in terms of the funded ratio (ratio of assets to pension liabilities). A municipality could have made 100% of its required contribution in 2016, and the fund could still be underfunded (and vice-versa).

In my April piece I identified municipalities that likely underfunded their police and fire pension funds between 2003 and 2010. Since publishing that piece I’ve gotten more recent data for a project I’m working on with Andy Crosby. As part of that project, I’ve been reading the audited financial statements for municipalities throughout Illinois, and—well, it’s been interesting.

As a note, I did not survey all local governments, so I cannot say whether the examples I discuss are common or unique to the municipalities mentioned. Further, I was largely focused on examining the financial reports for municipalities that according to data from the Department of Insurance (DOI) contributed less to their police and fire pension funds in 2016 than they were legally required to contribute. Table 1 highlights some relevant characteristics for the municipalities I discuss in this piece.

Table 1: Characteristics of Municipalities and Pension Funds Discussed

What stood out to me:

- No comparison of statutorily required pension contributions vs. actual payments.

I expected that municipalities’ financial reports would include the statutorily required pension contribution as well as what municipalities actually paid. That information is important because it would allow me to determine whether differences between actual contributions and required contributions in the DOI data were due to insufficient contributions or one of two other possibilities. As previously discussed, a difficulty in figuring out whether a municipality is shorting its pension systems is that differences between what a municipality paid and what the DOI said it should have paid may be attributable to misreported information and/or differences between actuaries. The latter is because state law allows a municipality’s required pension contribution to be determined by one of three actuaries: an actuary hired by the DOI, an actuary hired by the pension fund, or an actuary hired by the municipality. Differences in the assumptions actuaries use could lead to different pension contribution requirements being produced.

Some places’ financial statements did indeed allow me to figure out the reason for the discrepancy. The DOI’s data reported that the City of O’Fallon contributed $0 to its firefighters’ pension fund in 2016. However, O’Fallon’s 2017 audited financial report showed that it actually contributed more than $250,000 to the firefighters’ fund in 2016 (see p. 95 specifically). As such, the discrepancy between what DOI reported should have been paid in 2016 and O’Fallon’s reported actual contribution is attributable to misreported information and not actual underfunding.

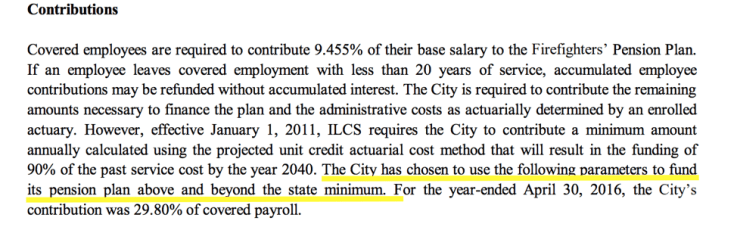

However, detailed information was absent in other municipalities’ reports. Using the DOI data, I determined that the City of North Chicago’s 2016 contribution to its firefighters’ fund was 55% of its required contribution. In examining its financial statement for 2016 I couldn’t figure out what accounted for the discrepancy, and oddly North Chicago states in that document that it funds its pension plan “above and beyond the state minimum” (see excerpt below).

Excerpt from City of North Chicago 2016 Audited Financial Statement (p. 72)

While North Chicago’s audited financial report states its pension payments are above state law requirement this was not the case in 2016 or 2017. Instead, North Chicago’s actual contributions were below what was legally required. As a result, the firefighters’ fund sent a certified letter to the Illinois Comptroller in April stating North Chicago shorted the fund, and requested that the Comptroller intercept state revenue and divert it to the fund to make up for that shortfall. In other words, despite the highlighted text quoted above, North Chicago did underfund its pension fund in 2016, and thus the DOI data was accurate.

- The Property Tax Extension Limitation Law hampers municipalities’ ability to properly fund their pension funds.

Non-home rule municipalities are subject to the Property Tax Extension Limitation Law (PTELL), and PTELL has important implications for a municipality’s ability to properly fund its pension systems. PTELL limits the amount that a municipality can increase its aggregate property tax levy from year-to-year to the lesser of 5% or the previous year’s Consumer Price Index. For reference, the 2015 CPI was just 0.7%, meaning a PTELL municipality could not increase its overall 2016 levy by more than 0.7% regardless of how its costs increased. The PTELL limit can only be overcome by a referendum, which must be approved by a majority of voters prior to the impacted levy year.

Many municipalities pay their required pension contributions with property taxes. Moreover, state law specifies that municipalities “shall annually levy a tax upon all the taxable property of the municipality at the rate on the dollar which will produce an amount” that’s sufficient to meet the state funding requirement. Some municipalities, however, use other revenue sources. The Village of Niles, for example, increased its sales tax rate in 2012, and part of the revenue from that increase is used for its pension contributions.

Regardless of the revenue source, state law mandates that municipalities pay into their police and fire pension funds an amount each year that is sufficient so that each fund has a 90% funded ratio by 2040. Importantly, this means that a municipality’s required contributions are tied to the pension fund’s financial condition. As a result municipalities’ payments will be higher for poorly funded pension funds and lower for well-funded ones. A downturn in the economy could, for example, dramatically decrease a pension fund’s financial condition, in-turn requiring higher municipality payments. Assuming a municipality uses the property tax to pay its pension contribution and is subject to PTELL, an increase in the pension contribution from the previous year that’s more than the lesser of inflation or 5% means it has to either a) cut some other aspect of its budget or b) get voters to approve a property tax increase above the PTELL maximum.

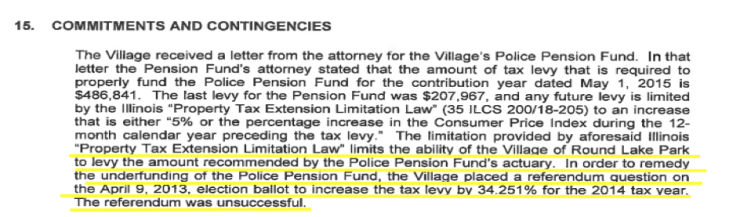

The Village of Round Lake Park’s required pension contribution increased by 6% from 2015 to 2016, but since it is impacted by PTELL the amount that Round Lake Park could increase its property tax levy by was a maximum of 0.7%. Several municipalities’ financial statements referenced an unsuccessful referendum. The example below is from the Village of Round Lake Park.

Excerpt from Village of Round Lake Park’s 2016 Audited Financial Statement (p. 65)

- Confusing explanation of the municipality’s required pension contribution.

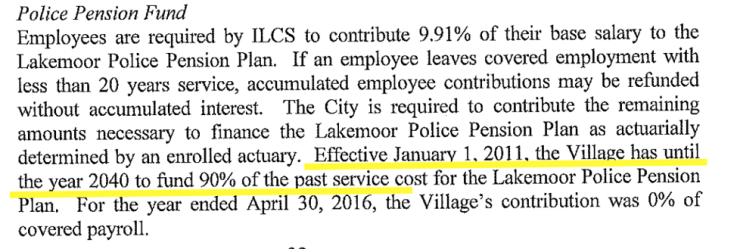

One thing I noticed is that several municipalities had an explanation of the state law governing their pension contributions that struck me as odd. The description of the state funding law included in the financial statements seemed to imply that the municipalities could underfund their police and fire pension funds so long as each had a 90% funded ratio by 2040. An example of the language is highlighted in the passage below, which is from the Village of Lakemoor’s 2016 audited financial statement (Crest Hill and Niles had identical language in their 2016 financial reports).

Excerpt from Village of Lakemoor’s 2016 Audited Financial Statement (p. 32)

The highlighted text above isn’t a totally accurate explanation of municipalities’ required pension contributions. State law specifies that a municipality’s annual contribution is to be:

equal to (1) the normal cost of the pension fund for the year involved, plus (2) an amount sufficient to bring the total assets of the pension fund up to 90% of the total actuarial liabilities of the pension fund by the end of municipal fiscal year 2040, as annually updated and determined by an enrolled actuary employed by the Illinois Department of Insurance or by an enrolled actuary retained by the pension fund or the municipality. In making these determinations, the required minimum employer contribution shall be calculated each year as a level percentage of payroll over the years remaining up to and including fiscal year 2040 (40 ILCS 5/3-125; 40 ILCS 5/4-118).

The law means that an actuary is supposed to determine each year what a municipality needs to contribute so the fund achieves a 90% funded ratio by the end of 2040, and it also requires that as a percentage of payroll contributions be the same from year-to-year (the actual dollar amount, however, will vary). Moreover, the 2011 law, as previously mentioned, put in place a new funding enforcement mechanism that allows the pension funds to request the Illinois Comptroller to send state revenue that would normally go to the municipality directly to the pension systems instead should the municipality’s annual contribution be less than what is required by state law. Lakemoor contributed 0% of what the Department of Insurance said it was required to pay to its police pension fund in 2016 (Lakemoor’s audited financial report verifies that no money was paid that year). In other words, Lakemoor did not pay its required pension contribution in 2016. As a result the pension board could request the Comptroller to intercept state revenue and divert it to the pension fund to make-up for the shortfall in Lakemoor’s 2016 contribution.

- Some municipalities have a pension funding policy that requires contributions greater than state law.

Ending with a positive, some municipalities have a funding policy that is stronger than state law. As previously mentioned, state law requires municipalities to fund their police and fire pension systems so that each one has a funded ratio of at least 90% by the end of 2040. However, a funded ratio of 90% means that a portion of pension liabilities are still unfunded, and the best practice is to strive for full funding (meaning obtaining a funded ratio of 100%). Some municipalities have chosen to implement a funding policy that aims for full funding, and as such their actual contributions are greater than the amount required by state law.

The City of Crest Hill, for example, has a policy to fully fund its police pension fund by fiscal year 2038 (see excerpt below). While paying off unfunded liabilities in a shorter amount of time requires higher contributions in the short-term it, in general, saves money in the long-term.

Excerpt from City of Crest Hill’s 2016 Audited Financial Statement (p. 11)

By aiming for full-funding and achieving that goal in a shorter time period, Crest Hill’s funding policy is stronger than what is statutorily required. As a result of its funding policy, Crest Hill’s contribution to its police pension fund in 2016 was 50% more than what the DOI reported was its required contribution was ($750 thousand required versus $1.125 million actual contribution).

Takeaway

So what’s my takeaway so far? First, it’s difficult to determine which municipalities are shorting their pensions each year, and you can’t just rely on the Department of Insurance data to figure it out. Same is true for identifying which municipalities have local funding policies that exceed the state pension funding law. Second, and related, it’s important to figure out why municipalities are shorting their pensions–is it because of PTELL, capacity issues, willful neglect, other items, or some combination? Also, how well informed are local elected officials of the funding enforcement mechanism and the state’s pension funding requirement? Last, I’ve clearly got a lot more work to do on this issue.