In digging into why the City of Chicago pays for CPS staff pensions (post about that is here), one thing that stood out to me was that jump in payment to the municipal fund (the MEABF) from budget year 2021 to 2022, shown in the chart below. “Wow, that seems a lot bigger than before” I thought to myself. I knew there was a jump from 2021 to 2022, but the increase seemed a lot higher than what I’d previously seen.

The City’s contribution goes from $576 million in 2021 to $930.2 million in 2022, that’s massive!

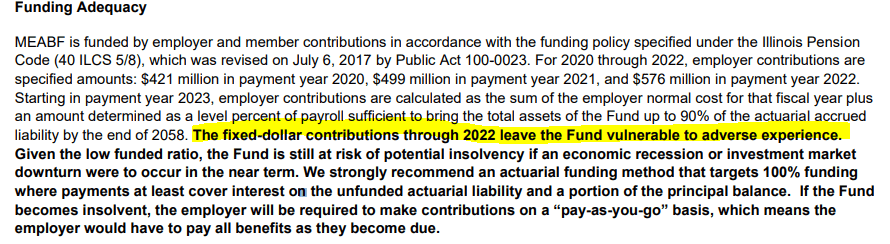

The dramatic increase is because budget year 2022 is the first year the City’s pension payments to the MEABF (and the smaller laborers’ fund) is actually tied to unfunded liabilities. For years 2017-2021 the contributions were fixed dollar amounts, set in state statute.

Why the fixed dollar amounts? The idea was that going from the way the city had historically funded its pensions to properly funding them was too expensive to do in one year. Instead, the Emanuel administration pitched having a “ramp period” in which the City’s contributions would increase over five years with the goal that by the end of the period switching to having the payments be based on actuarial calculations wouldn’t be that big of an increase.

The ramps created some short-term fiscal relief, but cost the City more in the long run and threaten the MEABF’s solvency.

There was a cost to the ramp periods though and now the jump in contribution between 2021 and 2022 is much higher than previously estimated. While the City’s payments for 2017-2021 were fixed, MEABF’s assets and liabilities were not. Liabilities increase as workers accrue benefits, and also increase/decrease depending on the accuracy of actuaries’ estimates and changes to assumptions. Assets also change with investment performance, as well as actuarial assumptions and changes. Since the funding law that created the ramps was passed MEABF’s funded ratio has decreased, sliding from 27.4% in 2017 to 23.3% in 2019. Erosion in the funding level increases the City’s required contributions. MEABF ‘s funding level is also so low it is at risk of insolvency, literally running out of money. The ramp period contributed to this risk.

Right now the City’s contribution to MEABF for 2022–the first ramp year–is estimated to be $930.2 million, a 62% increase from the 2021 contribution. Importantly, this more recent estimated is much higher than the estimate from when the new funding law was created. The MEABF’s 2017 financial report had the 2022 contribution at $853.5 million. In other words, the updated figure for the 2022 payment is $76.7 million more than initially predicted. MEABF’s valuation for 2020 isn’t out yet, so what the City owes for 2022 could be more or less than the $930.2 million figure. Whatever the final figure is for 2022, the City would have saved money in the long-run if there hadn’t been the ramps.

1 thought on “…About the Pension Ramps”

Comments are closed.