Last Wednesday, Chicago’s budget season kicked off with the release of the city’s 2022 budget forecast. I wrote about it in a previous post, highlighting what I saw as the three major items that will dominate budget discussions. One major item concerns Chicago’s nearly $1.9 billion in flexible (but not unrestricted) federal aid that it is receiving as part of the American Rescue Plan Act (or “ARPA”, for more on it read this or this). This post is about the Mayor’s proposal to use a portion of that aid to close the 2021 budget gap, and what it means in terms of the city’s finances, as well as the mechanics of the proposal. I focus on the mechanics some because the complexity of it is a reason why it’s difficult to understand exactly what is being proposed, which in-turn obscures the policy possibilities and stifles public debate.

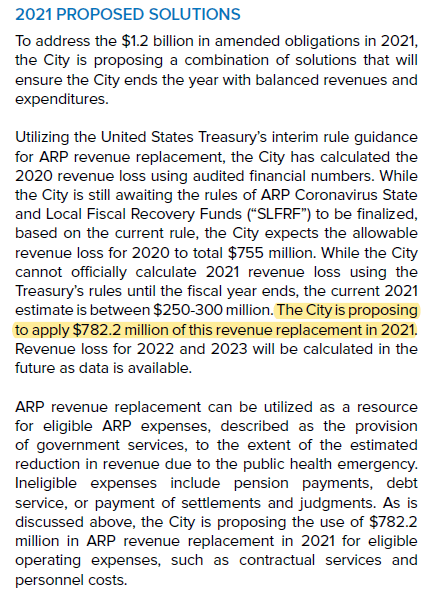

The budget forecast not only projects the city’s 2022 finances, but provides an update to the current, fiscal year 2021 budget. The city is now projecting that it has a $1.2 billion deficit in the current fiscal year, and a main way the Mayor is proposing to close that budget gap is to use a portion of Chicago’s ARPA aid. Here is how it is explained in the 2022 forecast document (emphasis added):

While the above passage states that the plan is to use nearly $800 million of Chicago’s ARPA aid on revenue replacement, implying that this federal aid will go to city spending that might otherwise be cut, the actual proposal is more complex. This is because Chicago already plugged its budget gap by taking out a line of credit (short-term borrowing). In a nutshell, the Mayor is proposing to use roughly 40% of Chicago’s ARPA funds to pay off that borrowing.

Who is the Mayor’s Proposal Being Marketed To?

Before digging into the details of what is being proposed I want to highlight who the plans are being communicated clearly to: the finance sector, and municipal bond market (or “muni market”) in particular. The city is essentially looking to promote this proposal as an example of how it is turning the fiscal ship and resolving Chicago’s long standing structural issues to the muni market.

And this promotion isn’t just about Chicago’s reputation, but can have material impacts in credit rating upgrades and lower borrowing costs. How (if at all) those would translate to tangible, on the ground impacts for everyday Chicagoans, particularly around greater investment in communities outside the downtown area and tackling long standing racial and economic disparities is an open question though.

One reason the Mayor’s ARPA spending plans are confusing for a general audience is that the discourse used to explain the plans is largely directed at the municipal bond market, including credit rating agencies, bank underwriters, and investors. For example, city officials explained the plans at an investor conference it hosted in May 2021. That event was an invitation-only virtual conference for “bondholders, real estate investors, and financial stakeholders” during which the city would provide the “municipal market” with insights into how it planned to use the ARPA aid. (side note: Rahm Emanuel held the first investor conference in 2011 and it was part of a larger effort “to improve communications with the financial community and boost investor interest” in Chicago.)

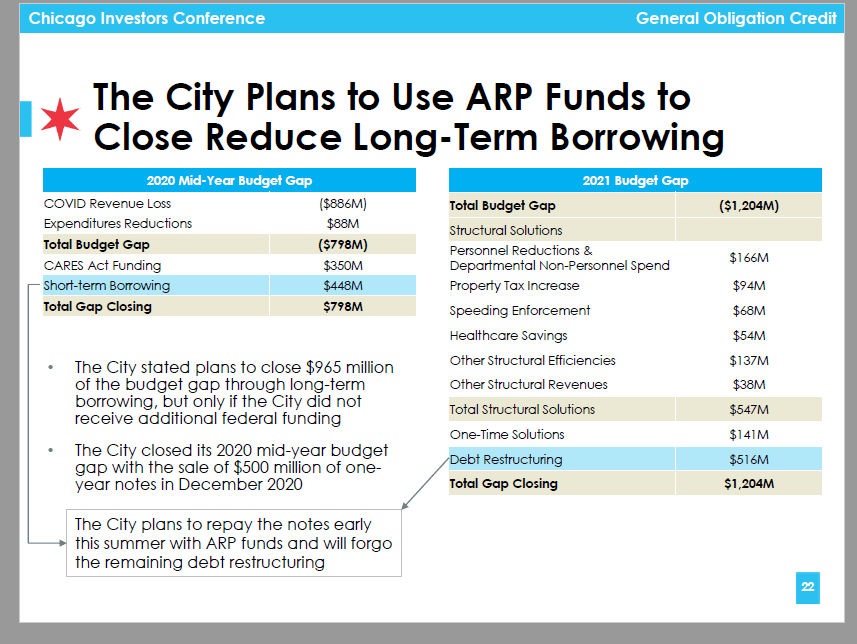

At the May 2021, investor conference, city officials made it clear that the Mayor is proposing to use 40% of Chicago’s ARPA funds to pay-off short-term borrowing and cancel long-term debt refunding and restructuring (or “scoop-and-toss”) that the City Council had previously approved (see a screenshot of the slide below).

Prior to the May conference, the Mayor’s strategy of using the ARPA money to pay off borrowing and avoid scoop-and-toss was reported in the Bond Buyer. While the Bond Buyer has been reporting on this plan, this information is only available to those with access to the newspaper and who understand the technical language of public finance.

The Bond Buyer is a specialty trade publication that is specifically for the municipal bond market. This means that unlike other outlets the Bond Buyer is written for a very specific audience, and the terminology used in it assumes readers have a familiarity with public finance and municipal bond market jargon that the average person doesn’t. In addition to the technical language, a subscription to the Bond Buyer is cost prohibitive for most people and is structured for institutional subscriptions (meaning the per person cost is discounted for companies that buy multiple subscriptions for their employees). An individual subscription to the Bond Buyer is much higher than other newspapers. For example, an individual Bond Buyer subscription is $720 per year, whereas a digital subscription to the Chicago Sun-Times is less than $100 a year.

How Is Chicago Proposing to Use ARPA Funds to Pay Off Borrowing?

The APRA spending proposal is connected to “$1.92 billion of refunding and restructuring of general obligation and Sales Tax Securitization Corp. debt” that the City Council authorized at the end of 2020. This larger refunding and restructuring deal is what’s referred to as “scoop-and-toss”, which is when old, outstanding bonds are paid off with new bonds, and overall debt payments are stretched out over a longer time period. This arrangement costs more in the long-run, but generates short-term, budget relief. It was a tactic Chicago used frequently under both the Daley and Emanuel administrations.

On December 18, 2020, the Bond Buyer reported that Chicago had finalized a short-term term borrowing deal (a line of credit) with J.P. Morgan as the lender. That borrowing had first been floated by Chicago’s Chief Financial Officer a month earlier and it was touted as a strategy to buy “the city up to one year to avoid a long-term, scoop-and-toss debt restructuring to fully close an $800 million gap due to COVID-19 pandemic tax wounds,” and that doing so “leaves the door open to scrapping scoop-and-toss debt restructuring should new federal COVID-19 pandemic aid come to fruition”. Importantly, this strategy was initiated at a time of uncertainty: after Joe Biden had been elected president, but before he was sworn-in and before Congress passed the American Rescue Plan. So the “time” the short-term debt provided the city was to see what the incoming Biden administration would do and whether more federal aid would be given to cities.

To put the plan differently, here’s how it all fits together: the COVID crisis resulted in significant, unexpected revenue loss for Chicago. To deal with that budget hole the Mayor could have made spending cuts and/or (theoretically) raised tax rates and fees to generate more revenue. The city’s revenue shortfall in 2020 was $755 million, which was nearly 20% of budgeted Corporate Fund spending. That amount exceeds total Corporate Fund spending on community services ($120 million), streets and sanitation ($153.8 million), and housing ($14.7 million). One thing to note is that this is only Corporate Fund spending, and some of these departments are supported with special funds too (the majority of the Public Health Department’s budget, for example, is from Grant Funds, and not the Corporate Fund). The revenue shortfall is also about 35% of the combined police and fire department budget. What portion of the city’s Corporate Fund spending is actually discretionary and could be cut is unclear (one lesson of Bruce Rauner’s governorship was that much of the state’s budget was not actually discretionary).

Instead of making dramatic mid-year spending cuts, city officials picked a different route: plug the budget hole with borrowing. Rather than taking on long-term debt, the city took out a line of credit with the hope that with a new president and new Congress, more federal aid would be provided to cities. Absent that federal aid, Chicago would convert that short-term borrowing into long-term debt. And the Mayor’s proposal is, ultimately, to use 40% of Chicago’s ARPA aid to avoid that conversion.

This proposed use of nearly half of Chicago’s ARPA aid, however, is not explained in plain language to the general public or even City Council members that have to vote on the budget (even for a public finance scholar like myself it was challenging to piece together). This opacity in turn suppresses debate about how to spend that money. The aid is a one-time, finite resource, so there necessarily has to be choices and tradeoffs with how to use it. The stakes need to be made clear though.

Who is Being Helped by this Proposal?

It’s important to center discussions on how to spend Chicago’s ARPA aid on who is being helped and how. Using one-time revenue to pay off debt can help bolster a government’s fiscal condition and generate long-term savings, but those financial logics and benefits don’t always connect to services, programs, or even a social mission (something I’ve written about before in the context of the Chicago Housing Authority’s use of “excess” reserves to pay off debt early; see also this report and this one). The Mayor’s proposal to use 40% of Chicago’s ARPA aid to pay off short-term borrowing and avoid increasing its long-term debt obligations.

While using the aid to pay off borrowing and avoid more scoop-and-toss might be fiscally prudent, that spending seems incongruous in a moment of crisis when many Chicagoans remain unemployed and thousands are behind on rent. The health and economic impacts have also been unevenly felt, with Black Chicagoans especially impacted. The uneven impact of the COVID crisis could lead to a deepening of existing inequities (something that occurred with the Great Recession). This isn’t to say that fiscal decisions should be made without thought to the city’s fiscal condition in mind, both today and in the future. The ARPA aid is a one-time resource, so if it is used to create new programs or expand existing ones the city will have to find a way to maintain that spending after 2024, when the ARPA funds run out. Fiscal policy needs to be tied to people and communities, and not just a city’s fiscal health in a vacuum.