Budget season kicked off in Chicago this week with the release of Mayor Lightfoot’s 2023 budget proposal. Chicago’s total 2002 budget is nearly $17 billion, and the budget consists of many different spending line items and funds (typically focus is on the Corporate Fund).

One item in the Mayor’s budget proposal that has caught a lot of attention is for Chicago to make “$242.0 million in advance payments towards future pension contributions” (see p. 20 of the 2023 budget overview).

What Exactly is this Advance Payment?

In nutshell the Mayor is proposing to contribute more money to Chicago’s four pension systems than is required by state law. Every year actuaries determine what the City needs to contribute to its pension systems based on state funding laws. The Pension Code requires Chicago’s annual contributions to be sufficient so that the police and fire pension systems are 90% funded by the end of fiscal year 2055 and 90% funded by the end of fiscal year 2058 for the laborers’ and municipal employees’ pension funds. Because of the funding laws the City is statutorily obligated to pay $2.37 billion to the four pension systems for budget year 2023.

You can think about this aggregate $2.37 billion payment as the minimum amount required. Under the Mayor’s proposal the City would contribute an additional $242 million above the statutory requirement. This would bring the total payment up to $2.61 billion (nearly a 15% increase from the 2022 payment of $2.28 billion).

What the Mayor is proposing isn’t entirely new. Cook County has also put more into its pension fund than required by law. The State of Illinois is also contributing more than is required by state law to its pension systems. However, these payments above what’s required are referred to as “supplemental” or “additional” payments. I’m not sure why Mayor Lightfoot uses the phrase “advancement payment”, but from what I’ve read it seems pretty identical to what Cook County and Illinois have done.

Why Would the City Pay More into the Pension Systems than is Required?

There are two main reasons for paying more than is required: reducing future costs and stabilizing the funds’ finances.

Potential Savings

The City’s pension payments are directly tied to the unfunded liabilities. Unfunded pension liabilities are a form of debt. But, unlike other forms of debt, unfunded liabilities are not a fixed amount, meaning the principal fluctuates from year-to-year (so too then does the interest). Pension liabilities are the value of benefits and assets are the money we have to pay benefits. Unfunded liabilities are the difference between liabilities (what we owe) and assets (money that we have to pay what we owe). Liabilities, however, represent an estimate of the value of benefits earned by people currently retired as well as current workers who won’t retire for decades.

To calculate unfunded liabilities actuaries have to project liabilities and assets decades into the future. Using those projections, actuaries also estimate what the City’s future payments will be, but these are just best guess estimates at one moment in time. The estimated savings from Mayor Lightfoot’s proposal are done by comparing what future payments would be with and without the City making that extra $242 million payment in 2023. All of this means that potential savings from the Mayor’s proposed “advanced payment” are contingent on a number of actuarial assumptions and projections.

Stabilizing the Pension Systems

The second reason for the advanced payment is to stabilize the finances of the pension systems. Combined, Chicago’s four pension systems are just 24% funded. For comparison, the State of Illinois’ five retirement systems are 42% funded (see Table 3). With this low level of funding there is a risk that the pension systems could become insolvent and run out of money. Right now even though they are poorly funded retirees’ benefits are not impacted and they continue to receive their pensions. If a pension system runs out of money this means it can’t send out benefit checks—an absolute nightmare scenario.

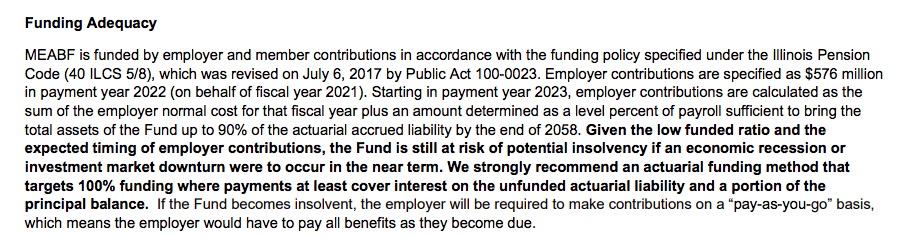

Tied to this is that Chicago’s pension systems are so poorly funded they run into a cash flow crunch. Meaning there’s a mismatch between money coming in and money going out for benefits. Because of this the pension systems sometimes have to liquidate investments and use that money to make benefit payments. This negatively impacts investment performance, which means less assets, which means worse finances. The pension systems’ actuaries have been explicit about this problem–below is an excerpt from the municipal employees’ 2021 actuarial repor

To put it bluntly, having to liquidate assets is another strain that can increase the risk of insolvency. Putting in more money now to Chicago’s pension systems now helps stabilize the pension systems’ finances.

I haven’t seen details in the proposal, so I am hesitant to weigh in on whether it specifically is prudent. That being said, given the low level of Chicago’s pensions systems, putting in more money than is required by state law is likely a wise move. Last, given that the City is in a position to put an additional $242 million into its pension systems another important question is, what other ways could that money be spent? That is beyond the scope of this blog, but is worthy of discussion as the 2023 budget is debated.

1 thought on “What Is Mayor Lightfoot’s “Advance Pension Payment” Proposal?”