I first started researching Illinois’ public pension systems in 2011. The 2010s was a high point for “pension crisis” rhetoric in Illinois (remember when Pat Quinn said he was “put on earth” to fix the pensions and Squeezy the Pension Python). Between 2009 and 2017, there was a flurry of legislative action to solve the “pension crisis.” (sidenote: I bristle at the phrase “pension crisis”) Major legislation was passed in 2010 that cut benefits for anyone hired on or after January 1, 2011 (this is known as the “Tier II” benefit). Multiple pieces of legislation also tried to solve the “crisis” by cutting benefits and were subsequently struck down by the Illinois State Supreme Court (SB1313 struck down in 2014; SB1 struck down in 2015; and SB1922 struck down in 2016). Despite all of that activity, most of Illinois’ public pension systems remain underfunded. While the focus on pensions has died down some it is still a topic that comes up around budget and election seasons. Whenever pensions come up I tend to do long (typo-filled) Twitter threads revisiting Illinois’ pension history. This time I thought it was time to write it all (or at least some) out in a more formal way. This is the first post in a planned series that will focus on the funding history of Illinois public pension systems.

There are hundreds of public pension systems in Illinois, and while there are some commonalities (again, most are underfunded), they each have their own histories. This blog focuses on the Chicago Teachers’ Pension Fund (CTPF). First thing to know is that the Chicago Board of Education (not the City of Chicago) is responsible for CTPF.

Another thing to know is that what the Chicago Board of Education (CBE) has to contribute annually to the pension fund is dictated by state law. So changing the funding laws requires action by the General Assembly and Governor. Of course the Mayor and local officials propose changes and lobby for and against legislation. Currently, the CBE has to pay into CTPF an amount that is sufficient to cover the cost of benefits earned by current employees (this is the employer share of the normal cost) and so that the pension fund will be 90% funded by the end of fiscal year 2059.

Third important thing to know is that the CTPF is nowhere close to being 90% funded. As of June 30, 2022, CTPF was 46.8% funded. The funding level (or “funded ratio”) is the ratio of assets (money to pay for benefits) to liabilities (value of benefits). A funded ratio of 100% means for every $1 in benefits there’s $1 in the bank to pay for it. Now, there’s actually a lot more that goes into calculating assets and liabilities, but I’m not getting into that here. Actuaries argue that prudent funding policy is striving for 100%, meaning that the funding target for the CTPF is below the typical standard (what the best funding policy is is also subject to debate, but that’s also beyond the scope of this post). There is also no funding level threshold or single metric to differentiate well-funded from poorly funded systems (some people use 80% as a standard, but that’s highly contested).

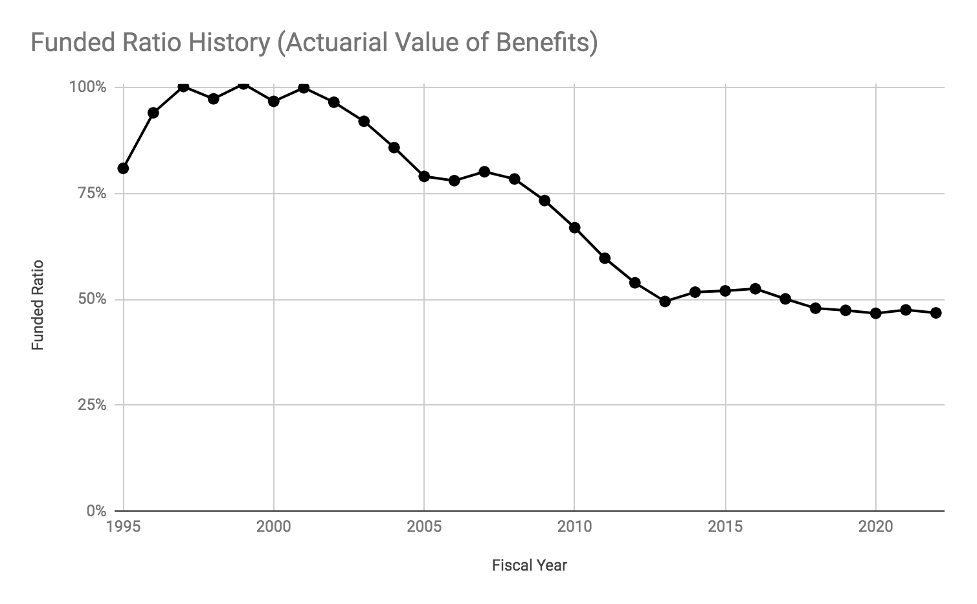

The CTPF, however, has not always had such low funding levels. The chart below shows the CTPF’s funding level between 1995 and today.

There are lots of factors behind why the CTPF’s funding level has deteriorated over time. The 2007-2008 recession was a big factor as pension systems around the country suffered double-digit investment losses. But the Great Recession is not the sole reason. A big factor has been insufficient contributions from the CBE. The remainder of this piece focuses on the funding law history and how, by design, the CBE underfunded the pension fund.

CTPF Funding History

The CTPF was well-funded for many years. As the chart above shows, between 1997 and 2002 its funding level hovered around 100%. So what happened? Well that story is tied to the larger story of Chicago Public Schools and its return to Mayoral control (for more see this article and book chapter I co-wrote; there’s also an entire dissertation on this topic). In 1995, the Chicago School Reform Amendatory Act (Public Act 89-15; the “1995 Act”) returned control of CPS to the Mayor of Chicago. More specifically it gave the Mayor power to appoint the school board (with city council approval) and hire the school district’s Chief Executive Officer. Remember, at this time CPS’s overall finances were in shakey shape and had been for years. CPS had a fiscal crisis in 1979/1980, which was resolved by the Chicago School Finance Authority taking over control.

The 1995 Act also consolidated CPS’s property tax levies and gave the CBE control over the allocation of property tax revenue. Prior to that change there had been a property tax levy dedicated to the CTPF—meaning property tax revenue went directly to the CTPF. Importantly, when control over the school district was returned to the Mayor state lawmakers didn’t also provide the district with increased revenue (something that was needed). Instead the consolidation of the property tax levies were meant to provide “financial flexibility”.

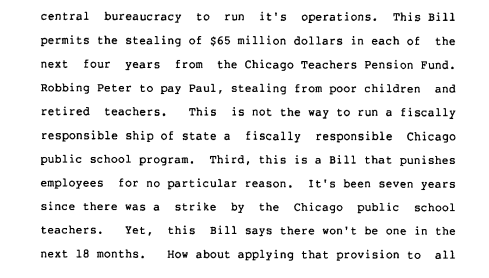

A final important thing the 1995 law did is that it changed the CTPF funding law and made it identical to the state pension systems’ pension ramp. Under this new funding law the CBE’s contributions to the CTPF, as a percentage of payroll, would increase between 1999 and 2010, and then from 2011 through 2045 the contributions would be sufficient so the CTPF would be 90% funded by the end of fiscal year 2045. The result was this cut how much money the CBE had to contribute to CTPF, freeing that money up for other uses. Representative Currie spoke out against this change during the House debate as highlighted in the passage below (p. 50 from the House transcript).

Then in 1997, subsequent state legislation (Public Act 90-548) was passed that changed how the CTPF was funded (another form of “financial flexibility”). The new provision specified that the CBE did not have to pay more into the CTPF than was required to keep the CTPF 90% funded, which meant that when the CTPF’s funding level was at least 90%, the CBE paid virtually nothing into the CTPF. This violates prudent pension funding policy in two ways. As previously mentioned, the industry standard is to strive for full funding. Second, this meant that the CBE wasn’t even covering the cost of benefits earned by current employees (the “normal cost”). The normal cost should always be paid. In a nutshell, rather than being paid for by annual contributions from the CBE these costs were being paid for with CTPF’s existing assets (and investment returns). It wasn’t until 2008, that the CBE’s contribution to CTPF covered the employer share of the normal cost.

The chart below compares the employer normal cost (again, the cost of benefits being earned each year) with the CBE’s actual contributions between 1996 and 2008 to highlight how little the CBE was paying into the CTPF. The CTPF characterizes the 1996-2005 period as a pension funding “holiday” and estimates that the holiday cost it more than $2 billion.

CTPF’s funding level was eroding in the early to mid-2000s. Once it dipped below 90%, the CBE’s required contributions to CTPF began increasing….and then the recession hit. Typically, there is a relationship between required contributions and a pension system’s funding level, so when the funding level tanks, required contributions increase. This was true for the CBE and CTPF, and absent any changes the CBE’s required contribution to the CTPF would have jumped in 2011. To be sure, the Great Recession caused massive fiscal challenges for the CBE (as it did for governments across the U.S.). In this fiscal crunch, the Mayor and the CBE turned once again to shorting the pension system.

As part of Public Act 96-889, the major legislation that created Tier-II (the reduced benefit tier for new hires), the funding policy for CTPF was changed. The legislation set the CBE’s contributions for 2011, 2012, and 2013 as fixed dollar amounts that were less than required under the previous funding plan. It also pushed the target for reaching the 90% funding level from 2045 to 2059. This amounted to a pension funding holiday. Under the old funding law CBE would have had to contribute nearly $600 million to CTPF in 2011, and PA 96-889 slashed the required contribution to just $187 million.

There was another attempt to reduce the CBE’s required pension contributions in 2013. SB 1920 would have cut the CBE’s required contributions for an additional two years (for 2014 and 2015 specifically) by hundreds of millions of dollars, but Governor Pat Quinn vowed to veto any pension holiday legislation.

A major point is that you can’t understand CTPF’s woes without situating it within the larger changes to the CBE and its financial challenges. Getting into the CBE’s wider financial issues is beyond scope for this blog. If you’re interested in this topic I highly recommend this article by Dr. Stephanie Farmer and Dr. Rachel Weber.

One final thing to know about CTPF. Its underfunding isn’t all because of the CBE. The state pension systems’ funding law was set in 1996 by Public Act 89-593. Prior to that Act, the state had contributed money to the CTPF, and the amount that it contributed was between 20% and 30% of the state’s annual contribution to the Teachers’ Retirement System (the pension system for all non-Chicago teachers). That amount was around $60 million. A provision of PA 89-593 stated that it was the intention for the state to continue contributing to CTPF what it historically had, which could be interpreted as 20-30% of the TRS contribution. However, because the word in the legislation was intent this meant the state was under no legal obligation to make those payments to the CTPF (something legislators state explicitly during the Senate and House floor debate) and the state didn’t end up making those payments.

Updated additional thoughts (added March 5, 8PM PT)

Patrick Leow pointed out some additional items to me on Twitter that are worth mentioning, although digging deeply into them (or other aspects of CPS’s and CTU-CPS’s histories) is beyond the scope of this post.

First, Public Act 90-852 (technical revisions done by PA 90-655 and PA 91-0357) implemented benefit changes for members of the CTPF and Teachers’ Retirement System in 1998. A main thing was that it changed the formula for calculating retirement benefits, thereby increasing benefits (there are other changes too that I don’t get into). It also increased employees’ required contribution to CTPF from 8% to 9%. The state and CBE were also required to contribute small percentages of payroll for the benefit increases. I haven’t seen any analysis evaluating whether the increased contributions from employees, the state, and the CBE were sufficient to cover the benefit increase costs.

Second, while employees’ contribute 9% of salary for their CTPF retirement benefit, the school district “picked-up” the majority of those required contributions and had done so for decades. Of employees’ 9% required contribution, the district paid 7 percentage points and the remaining 2 percentage points came from employees’ actual salary. Ending the pick-up was a part of the 2015-2016 contract negotiation, and eventually a deal between CPS and the Chicago Teachers Union was struck.

An important takeaway from this post is that the deterioration of the CTPF’s funding level is not attributable to one sole action or actor.

Another Update (Added March 7)

In 2016, state lawmakers approved Public Act 99-521, which reinstated a property tax line that is dedicated to the CTPF (the “Special Pension Property Tax Levy”). That new line took effect starting in fiscal year 2017, and capped the rate at 0.383%. Then, in 2017, state lawmakers overhauled how the state provides funding for K-12 education in Illinois in 2017. The relevant legislation is Public Act 100-465, which created the Evidence-Based Funding formula. For the CTPF, two relevant parts of that law are 1) it requires the state to pay for the normal cost (again, the cost of benefits earned by current employees); and 2) it increased the maximum rate for the Special Pension Property Tax Levy from 0.383% to 0.567%.

2 thoughts on “Pension Funding History Series: Part I – The Chicago Teachers’ Pension Fund”

Comments are closed.